Red Chilli Powder: A Guide to Varieties, Grades, and Global Trade

"Red Chilli Powder" is a global B2B trade commodity, made by grinding ripe and dried 'Capsicum Fruit Pods' into a single-ingredient powder. The commodity is valued by food manufacturers for its two key characteristics: 'heat' as a result of its 'capsaicinoid' content and 'colour' as a result of its 'carotenoid' composition, where quality is quantified by 'ASTA' units. While it's commonly referred to as 'crushed chillies' or 'crushed peppers' across retail platforms, high-grade 'chilli powder' for international exports goes beyond that, with effective processes employed for its manufacture. For one, 'chilli variety' is chosen for its perfect mix of 'red colour' and 'heat'.

This pure powder can be considered an important raw material for both HORECA use as well as general food production. It's made via a basic process that requires drying the chillies and eliminating moisture before grinding them into a powder. This single-ingredient form makes Pure Red Chilli Powder different from a blended version known as “Chilli Seasoning” that contains fillers such as cumin or even salt. The functionality of this product is quite basic, adding natural heat to certain recipes such as curry, as well as providing a certain red colour seen in dishes such as Tandoori chicken.

PRODUCT SPECIFICATIONS

Parameter

Standard / Limit

Purity

100% dried fruit of Capsicum annuum / C. frutescens

Critical Note: Specifications for ASTA (Colour) and SHU (Heat) vary by grade. Buyers must specify target values (e.g., ASTA 60-140) in the purchase order.

TYPES, GRADES & VARIANTS

In the red chilli powder B2B trade, Red Chilli Powder is strictly segmented by its physicochemical profile, specifically referencing Scoville Heat Units (SHU) for pungency and American Spice Trade Association (ASTA) values for colour intensity.

Kashmiri (Premium Colour): High-value, low-pungency (10k-12k SHU), ASTA 100+ for exceptional colour. Preferred by red chilli powder exporters in India and "clean label" products for visual appeal, replacing synthetic dyes.

Guntur Sannam (Commercial Standard): Benchmark variety (35k-40k SHU) for Red Chilli Powder Exports. Dominant in global supply chains for consistent heat, used widely in sauces, blends, and mass-market foods.

Teja / S-17 (High-Heat Extraction): Intense pungency (75k-100k SHU). Primary feedstock for oleoresin extraction, pharmaceuticals, and concentrated hot sauces, valued for cost-effective heat yield.

Byadgi (Balanced Profile): The "sweet spot" with high colour (like Kashmiri) but with more bite. Essential for specific regional/South Indian cuisine and masala blends, offering the dual advantage of deep colour and distinct flavour.

APPLICATIONS & END-USE MAPPING

Food Processing (Industrial)

Meat & Poultry This product functions as a natural colouring agent, replacing synthetic colours. The colours find application in natural processed meats such as sausages, salamis, tandoori marinades, and achieve high grades of ASTA, thus providing a bright appearance to the food, giving the consumer a perception of freshness.

Sauces & Condiments The spice is a primary feedstock for the wet condiment industry, providing foundational flavour and establishing consistent heat levels in hot sauces and ketchups. It is also a key component in the dry "tastemakers" or seasoning sachets for instant noodles, adding instant pungency.

Snacks In the dry snack market, the product is engineered for uniform dispersion and adhesion. It is used as a seasoning dusting for chips, nuts, and extruded snacks. Particle size is optimised for surface stickiness, ensuring consistent flavour, colour, and "mouthfeel" in every bite.

Oleoresin & Nutraceuticals

Extraction The crop is processed for chemical isolation to produce high-value Oleoresins, which are concentrated, standardised extracts. Oleoresin Capsicum is extracted for pure pungency ("heat") in food, and Oleoresin Paprika for a stable, oil-soluble, heat-stable natural red colourant.

Pharma In the realm of the drug and wellness space, the focus has been on extracting the bioactive compound Capsaicin, which has found application in analgesic creams and patches useful for relieving localised pain, like sore muscles and arthritis, and nutraceuticals with weight management properties due to the thermogenic effect of Capsaicin on metabolism.

Retail & HORECA

Culinary (Retail) Priced as a must-have kitchen essential for the everyday home cook, this spice adds depth, vibrancy, and intensity to the home cook's go-to curries, stews, and marinades. Emphasis is given to the fresh quality and aromatics on marketing packages intended for home use.

Food Service (HORECA) This segment is in need of the same quality of performance in an efficient, bulk format that is intended for the high-volume institutional kitchens. The emphasis is on performance and reliability in whipping up hundreds of meals a day.

SUPPLY & DEMAND COUNTRIES (GEO + TRADE)

Top Producing Countries & Export Hubs

Production Leaders With a staggering 35-40% market share, India rules the world stage. With the help of China, Thailand, Ethiopia, and Pakistan, it stabilises regional availability by anchoring the global supply chain.

Key Export Hubs The trade is centralised in specific zones. India's Guntur region (along with Khammam and Warangal) acts as the primary global price-setter and aggregation point. China complements this as a major export hub, competing largely in bulk volumes.

Key Export Hubs The trade is centralised in specific zones. India's Guntur region (along with Khammam and Warangal) acts as the primary global price-setter and aggregation point. China complements this as a major export hub, competing largely in bulk volumes.

Top Importing Regions

Asia China acts as a unique hybrid market; despite high domestic output, it imports vast quantities of high-heat Indian chillies specifically for industrial processing. Malaysia and Thailand also remain heavy importers to supplement local culinary demand.

North America The USA is the largest single buyer for value-added products. Unlike markets buying raw whole spices, the US demand focuses on processed powder and flakes to support its massive industrial food and snack manufacturing sectors.

Middle East The UAE and Saudi Arabia form the regional entry points and distribution hubs. Despite strong demand from the local market, the UAE is primarily a strategic re-export centre, transshipping large imports into smaller GCC markets and North Africa.

Europe The UK and Germany drive this demand for quality. Tight regulatory guidelines, specifically free requirements of Aflatoxin and standards of IPM, epitomise this market, translating into higher margins for the clean and traceable produce.

GLOBAL MARKET OVERVIEW

Current Market Valuation: Estimated ~USD 1.7 Billion (2024) [Source: Market Research Reports].

Forecast: Expected to reach USD 2.6 - 2.9 billion by 2030-2032.

The Heat phenomenon is here to stay. There is a global taste for more robust, pungent flavours, and high-SHU chillies are moving from specialist shelves to mainstream kitchens as spicy food cultures, such as Indian, Mexican, Thai, and Sichuan, come into vogue.

The clean-label revolution is quietly revolutionising the chilli industry. Consumers are demanding less artificial stuff, and natural dyes are on the up. Paprika and Kashmiri chillies provide a consistent, vibrant red colour that is a reliable, clean-label substitute for artificial dyes such as Red 40.

Chilli is a super-ingredient for the flavour and fragrance industry. Oleoresins, highly concentrated liquid extracts, are flying out of the door because they provide consistent heat and colour that large-scale food production requires for sauces, snacks, and seasonings.

PRODUCTION & SUPPLY DYNAMICS

Production Leader: India is the undisputed leader, controlling price discovery through the Guntur (Andhra Pradesh) market.

Seasonality:

Harvest (India): February to April (Peak arrivals).

Lean Season: June to December (Supply from Cold Storage).

Risks:

Climate: Unseasonal rains during drying can spike moisture levels, leading to fungal (Aflatoxin) issues.

Pests: Thrips (invasive pest) outbreaks can severely impact crop yield and visual quality.

International Trade Patterns & Regional Outlook

India → China (Industrial Volume): Due to China's demand for affordable, high-heat Indian varieties like Teja (S17), this is the route with the greatest volume. China increases the competitiveness of its domestic manufacturing by using these imports for the industrial extraction of paprika and capsicum oleoresin.

India → USA/EU (Quality & Compliance): This high-value route prioritises quality over quantity. Western markets demand strict adherence to low pesticide and pathogen standards, requiring premium grades such as IPM and steam-treated batches. The largest profit margins are found in this corridor.

Re-export Hubs (Strategic Intermediaries): Two important distribution hubs are Vietnam and the United Arab Emirates. Vietnam is a key trade logistics hub, re-exporting Indian chillies, mainly to China and Southeast Asia. The UAE (Dubai) acts as the Middle East's repackaging hub for African and difficult-to-access markets due to its central location.

EXPORT & IMPORT TREND ANALYSIS

Volume Trend: Consistent year-on-year growth (~3-5%) driven by population growth and changing palates in the West.

Value Trend: Rising. Quality compliance costs (lab testing, sterilisation) and higher input costs are pushing unit prices up.

Key Insight: Buyers are increasingly bypassing traders to source directly from processors in origin countries to ensure traceability and lower Aflatoxin risks.

PRICE & BULK COST INDICATORS

Standard & High Heat Grades

Base export varieties (Medium Heat) generally range between $2,200 to $2,800 per metric ton. The industrial varieties of High Heat (considering Teja/S17) maintain a stronger position, ranging between $2,600 to $3,200 per MT, supported by consistent demand in the extraction and processing sectors.

Premium & Organic Markets

Speciality varieties prized for intense colour, such as Kashmiri and Byadgi, trade at a significant premium of $3,500 – $5,500 per MT. Organic certification further escalates value, adding a 20% to 30% surcharge on top of these standard rates.

Market Volatility

Note: Figures are indicative for Q4 2024 - Q1 2025. Actual pricing fluctuates weekly, heavily dependent on Guntur mandi arrivals, cold storage stock levels, and currency exchange rates.

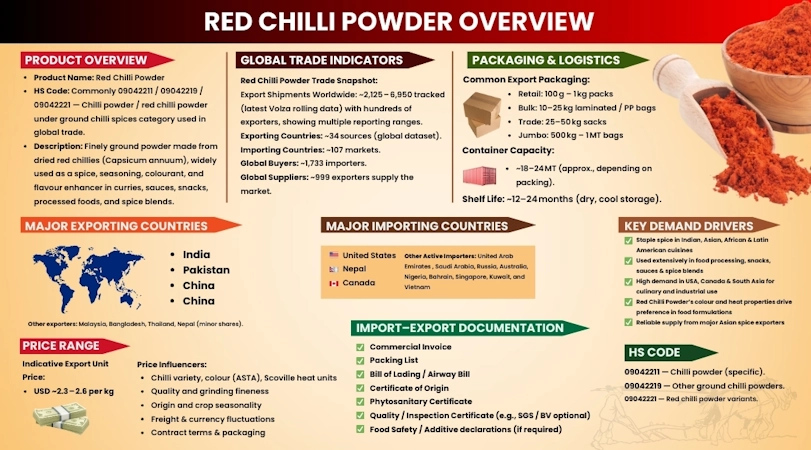

HSN / HS CODE & TAX CLASSIFICATION

HS Code (Global): 0904.22 (Fruits of the genus Capsicum... Crushed or Ground).

Indian HSN Code:

0904 22 11: Red Chilli Powder (General / Standard).

0904 22 19: Other (Speciality / Blends).

Taxation: Subject to GST (in India) and Import Duties (variable by destination country). Essential for calculating Landed Cost (CIF).

BUYER EXPECTATIONS & TRADE REQUIREMENTS

Sudan Dye Free: The #1 deal-breaker. Buyers require a "Certificate of Analysis" (CoA) proving zero detection of Sudan I-IV.

Aflatoxin Control: EU buyers demand < 10ppb. US buyers demand < 20ppb. Sourcing from IPM farms is often required.

Mesh Size Consistency: Industrial buyers need exact particle size (e.g., 60 mesh) to ensure the powder blends legally into sauces/mixes without clumping.

Colour Stability: Guarantee that ASTA values won't drop significantly during shipping (requires good barrier packaging).

Logistics, Packaging & Trade Terms

Packaging Standards We protect spices from losing their essential oils and colour by providing solid packaging. For bulk purchases, we provide 25 kg or 50 kg poly-lined HDPE bags to prevent moisture and clumping. For retail and Food Service (1-10 kg) sales, the emphasis changes to branding and shelf life, so we provide Aluminum Foil Pouches or multi-layer Kraft Paper bags that protect against UV and oxidation.

Storage & Shelf Life The inventory should be kept in cold storage at a temperature lower than 15°C to preserve commercial-grade and ASTA colour. This will delay the degradation of colour and help extend the shelf life up to 12-18 months.

Incoterms & Documentation Incoterms vary based on the buyer's experience level. For experienced buyers of bulk spices, FOB (Chennai/Mundra) is the norm; however, since CIF shifts the risk of ocean transport and insurance to the seller, it might be more suitable for inexperienced importers. The Bill of Lading, Invoice, Packing List, Phytosanitary Certificate, and Certificate of Analysis (CoA) are among the documents required for customs clearance.

Regulatory Compliance & Certifications

Mandatory & Market Access

Operating at baseline involves adherence to national norms—FSSAI for domestic sales, Spices Board of India registration for exports—and obtaining a Phytosanitary Certificate for every consignment. However, for entry into high-paying international markets, there is a need for more extensive compliance. The USA demands FDA Registration and FSMA compliance, while Europe is very particular about chemicals, demanding pesticide residue clearance (tested by labs like Eurofins or SGS) and REACH compliance.

Premium & Value-Add Standards

For securing major contracts with global food giants, most “Optional” standards become de facto mandatory. Advanced quality management is demonstrated by food safety standards such as BRC or FSSC 22000. Organic (USDA/EU), Halal, and Kosher standards are crucial differentiators that enable premium pricing and entry into exclusive retail markets.

Future Outlook & Opportunities

The spice market is shifting from generic blends to Single Origin Powders, valuing "terroir-based" marketing (e.g., "Guntur," "Kashmiri") for educated consumers.

Cryogenic Grinding (freezing with liquid nitrogen before milling) is setting new quality standards. This "Cold Ground" technology prevents heat damage, retaining up to 95% of essential oils and flavour, offering a more potent product than traditional hammer milling.

Traceable supply chains, from farm to fork, are now a requirement for entry into the EU and US markets. Large retailers are now requiring complete digital visibility to ensure ethical labour practices and sustainable farming practices, making traceability a key priority for entry into these markets.

TRANSPARENCY & DISCLAIMER (EEAT)

Disclaimer: Market data, price indications, and trade regulations may change because of harvest conditions, geopolitical policies, and currency fluctuations. The technical details are for general guidance only; buyers must verify the details (ASTA, SHU, Pesticide Limits) with suppliers through a Certificate of Analysis (CoA) before making a purchase. No specific trade result can be guaranteed by Tradologie.

We use cookies to enhance site functionality, improve user experience, analyze website performance, and deliver relevant content in accordance with our Cookie Policy.

We use cookies

Essential Cookies

Essential cookies are strictly necessary for Tradologie.com to operate properly. They enable core functionalities such as security, session management, network stability, and cookie consent preferences. These cookies do not collect personal data and cannot be disabled.

Name

Vendor / Service

Purpose

Expiry

Privacy Policy

ASP.NET_SessionId

Tradologie.com / ASP.NET

Maintains secure user session across pages.

Session

https://privacy.microsoft.com/

__RequestVerificationToken

Tradologie.com

CSRF protection for forms.

Session

https://www.tradologie.com/privacy-policy/

cookie_consent

Tradologie.com

Stores consent preferences so the banner does not reappear.

We use analytics cookies to gather anonymous, aggregated information about how visitors interact with Tradologie.com. This helps us improve the site, measure the success of content and services, and prioritize performance fixes.

Functional cookies allow the website to provide enhanced usability and personalization. They store preferences such as language, region, chat settings, and login details for a smoother browsing experience. Disabling these cookies may limit certain features.

Name

Vendor / Service

Purpose

Expiry

Privacy Policy

user_lang / lang

Tradologie.com

Remembers chosen language.

1 year

https://www.tradologie.com/privacy-policy/

timezone_pref

Tradologie.com

Stores timezone preference for display.

6 months

https://www.tradologie.com/privacy-policy/

remember_user

Tradologie.com

Keeps logged-in state when chosen.

30 days

https://www.tradologie.com/privacy-policy/

livechat_session

Tawk.to

Maintains chat session state.

Session

https://www.tawk.to/privacy-policy/

Marketing

Marketing cookies are used to deliver advertising that is relevant to you and to measure the effectiveness of our marketing campaigns across platforms such as Google, LinkedIn, Meta and Microsoft. These cookies are set only with your consent.