Global agricultural trade moves on invisible gravity. When the vast production engines of the Western Hemisphere accelerate simultaneously, the ripples are felt on every grain desk from Chicago to Odessa. We are currently witnessing one of those structural realignments. A combination of an upgraded South American harvest and an aggressive, rhythmically flawless spring planting campaign in the United States is rapidly shifting the global soybean balance sheet from tight anxiety to absolute cushion.

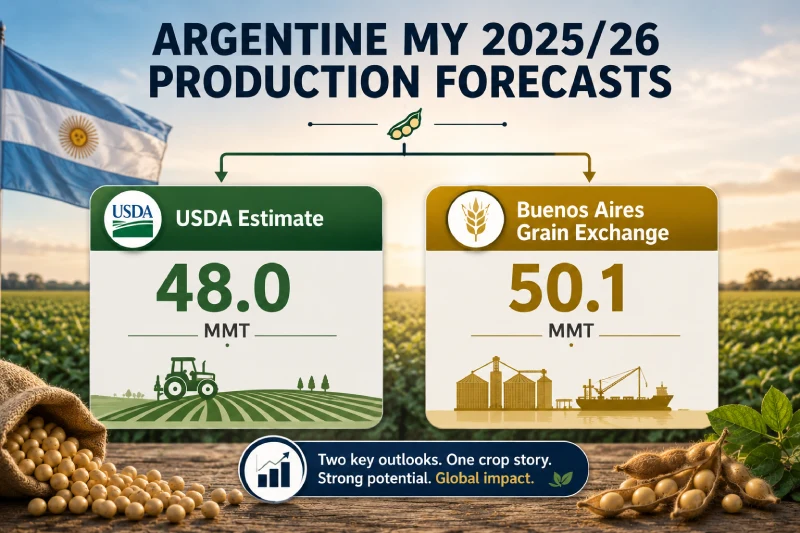

The numbers coming out of the southern fields tell a story of remarkable resilience. Over in Argentina, where the combine harvesters have already eaten through nearly three-quarters of the planned area, the fields are yielding an exceptional surprise. Analysts at the Buenos Aires Grain Exchange just pushed their production dial upward, raising the crop forecast from 48.6 million metric tons to a comfortable 50.1 million tons. For context, that outpaces the current USDA baseline by more than two million tons. This is not just a statistical victory; it is a physical reality driven by an average yield of 3.28 tons per hectare—the highest productivity the Argentine pampas have registered in six seasons.

Simultaneously, Brazil’s export conveyor belt shows no signs of slowing down. The local agency ANEC estimates that May will see a massive 15.9 million tons of Brazilian beans exit their ports. While technically a breather from April’s record-shattering 16.75 million tons, this volume sits a staggering 2 million tons above what Brazil managed in May last year. When you pile these South American totals on top of a lightning-fast US planting season—where farmers have already drilled 79% of their planned acreage compared to the 68% five-year average—the speculative premium simply evaporates.

Traders at the Chicago Board of Trade are doing what they do best: pricing in tomorrow's abundance today. July futures dropped 3.8% in a fortnight, stabilizing at $435.5 per ton. The long-term speculative buyers have left the building, safe in the knowledge that total availability is guaranteed unless a severe North American summer drought emerges to break the bearish spell.

The Ukrainian Anomaly: A Local Bull in a Global Bear Market

Look away from the board in Chicago, however, and the view changes completely. In Ukraine, the oilseed market is operating on an entirely different set of economic physics. Local prices are refusing to follow the international downward slide, holding onto a stubborn, defensive premium that isolates domestic crushers from the global collapse.

At the factory gates, crushers are fighting a quiet war for physical volume. Farmers are holding their remaining beans tightly, well aware that domestic processing capacity is hungry. Purchase prices for genetically modified (GM) soybeans have dug in at 21,700 to 22,000 UAH per ton ($430–$440 excluding VAT). But the real drama is playing out in the identity-preserved, non-GM sector. Over the past week, domestic non-GM prices climbed another 200 to 300 UAH, hitting 22,500 to 22,700 UAH per ton delivered to plant.

This is an island of bullish sentiment. Outbound ocean freight for GM beans at the deep-water ports has gone quiet, but European demand for certified non-GM varieties is acting as a powerful vacuum. For deliveries headed straight to Ukraine's western land border, European buyers have bid prices up by another $5 per ton in a single week, setting the current target at $480 per ton.

The export numbers prove that the Black Sea logistics channels are working hard. By May 21, monthly soybean exports reached 172.9 thousand tons, easily outstripping April’s total of 158.5 thousand tons. This pushes the season’s cumulative volume to 1.82 million tons. Turkey remains the largest single destination, taking 58.4 thousand tons, followed by a steady European line including France (33k tons), the Netherlands (28.4k tons), and Germany (12.5k tons). Furthermore, Ukraine is successfully exporting value-added products, moving 31.1 thousand tons of soybean oil and 93.1 thousand tons of meal this month alone.

But this local isolation cannot last forever. As Argentine crushing mills accelerate and begin pouring massive volumes of meal and oil into European ports, this high-priced Ukrainian defensive pocket will inevitably face severe commercial gravity.

The Crushing Shift: Changing Dynamics in European Feed Infrastructure

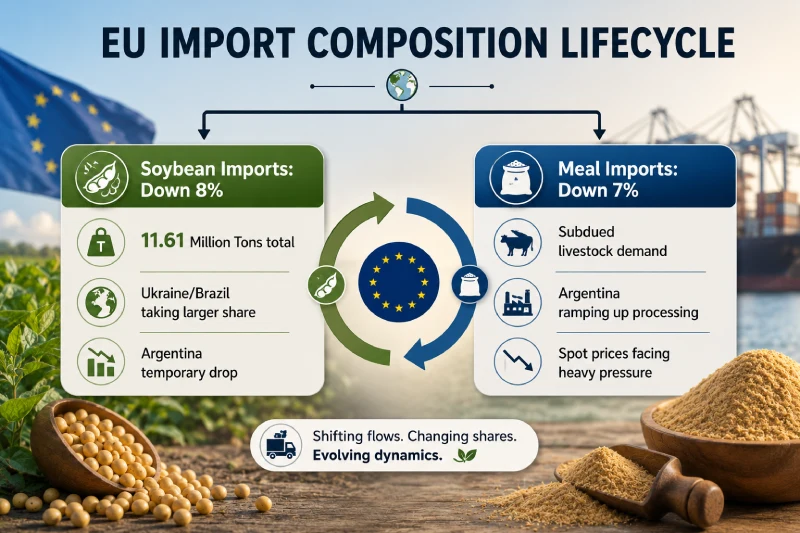

The European Union is transforming into a textbook buyer’s market. European Commission data shows that as of mid-May, total EU soybean imports for the season dropped 8% compared to last year, cooling down to 11.61 million tons. More importantly, the import of processed soybean meal fell 7%, reflecting a quiet, subdued demand environment across continental livestock and poultry complexes.

Up until now, Brazil and Ukraine have been capturing a larger slice of this smaller European pie, while Argentina’s share temporarily dipped. That landscape is about to turn highly competitive. Argentina’s unique structural advantage is that its agricultural economy is engineered to export processed products—meal and oil—rather than raw, unrefined beans. With an extra 1.5 million tons of upgraded harvest land moving into Argentine crushing plants, a wave of highly competitive meal is about to hit international trade routes.

For European feed compounders, poultry integrations, and dairy operations, this represents an exceptional shift in bargaining power. Spot prices across European distribution hubs face a steady ceiling. Importers can now afford to negotiate aggressively, playing alternative supply lines against one another.

Macro Trajectories and Strategic Scenarios

The broader oilseed complex is currently locked into a bearish-to-neutral holding pattern that will likely dictate the next one to three months. Abundant spot shipping out of Santos, an upgraded processing outlook from the River Plate, and a flawless start to the US crop year mean that global buyers are facing zero immediate supply anxieties.

The long-term multi-functional online platforms, such as UkrAgroConsult’s AgriSupp platform—which tracks real-time historical data, analytical reporting, and daily operational numbers across the Black Sea and Danube markets—confirm that the supply buffer is historically secure.

Global Supply and Demand Projections (2025–2031)

The structural shift across the broader foodservice and agricultural input landscape is best reflected by evaluating long-term market size trajectories. According to recent institutional industry data, the broader Africa and global foodservice supply network is scaling along a steady path:

| Performance Metric | Historical Floor (2025) | Operational Base (2026) | Long-Term Forecast (2031) | Expected Sector CAGR |

|---|---|---|---|---|

| Market Valuation Layer | USD 75.92 Billion | USD 79.81 Billion | USD 102.43 Billion | 5.12% |

Source: Mordor Intelligence - Regional Foodservice Market Analytics.

What could break this bearish trajectory? Three distinct catalysts have the power to rapidly reverse this downward momentum:

- North American Summer Weather Stress: This is the single most critical variable. If the current favorable conditions give way to an intense, persistent ridge of heat across the US Midwest during the critical pod-filling stages of July and August, yield expectations will drop instantly, triggering an aggressive short-covering rally.

- A Change in Chinese Import Velocity: China consistently commands more than 60% of the world’s traded soybean volume. A sudden acceleration in their bulk reserve purchases from the US or Brazil would rapidly tighten port availability.

- Biodiesel Demand Acceleration: Any policy shift that increases the blending mandates for renewable diesel or aviation biofuels would immediately drain the global soybean oil pool, forcing crushers to buy beans strictly to satisfy energy markets.

Strategic Sourcing Recommendations

For commercial procurement desks, the operational roadmap requires a split strategy. International buyers can afford to run lean inventory setups, utilizing the current South American supply wave to keep spot costs low and letting the market carry the storage risk.

For Ukrainian exporters and domestic processors, the reality is far more time-sensitive. The current price premium for non-GM varieties at the western borders represents an excellent commercial window that will inevitably narrow as South American processed options arrive in volume. Locking in sales margins now, before the full weight of the North American crop hits the global balance sheet in autumn, remains the most prudent path to navigate this gathering wave of global abundance.