Key Highlights

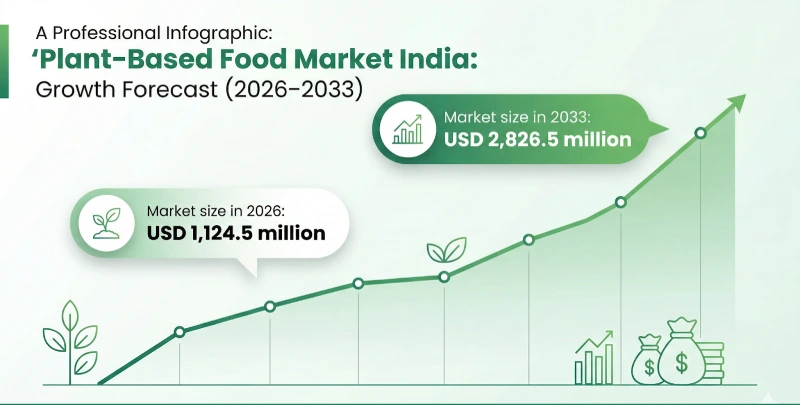

- India's vegan food market reached USD 1,124.5 million in 2026 and is projected to hit USD 2,826.5 million by 2033.

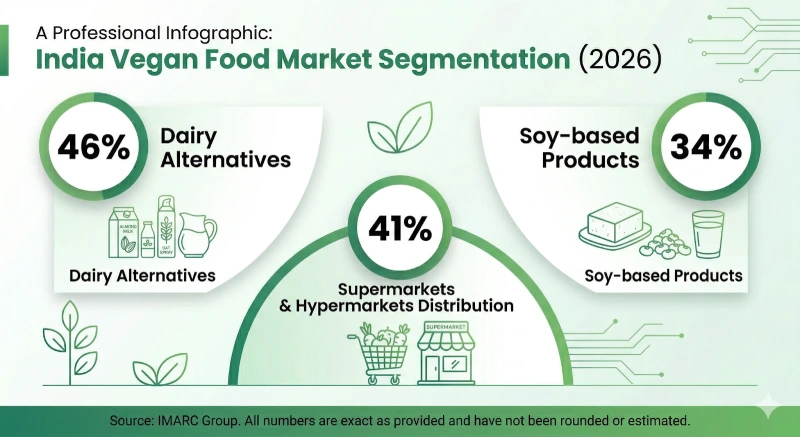

- Dairy alternatives dominate with ~46% market share, led by almond and oat milk.

- Soy remains the leading ingredient with ~34% share in plant-based products.

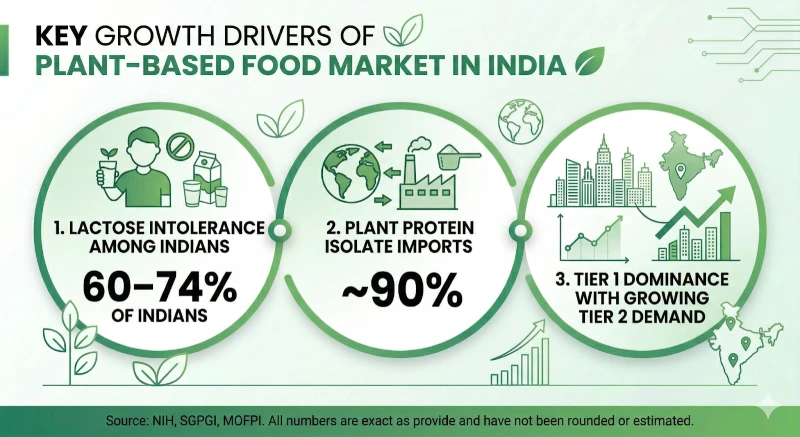

- Around 60–74% of Indians are lactose intolerant, driving demand shift.

- India imports ~90% of plant protein isolates, showing strong B2B opportunity.

- Tier 1 cities dominate demand, but Tier 2 markets are rapidly growing.

- Growth is driven by health awareness, sustainability, and flexitarian diets.

Intro:

Plant-Based Food Market India 2026: Size & Growth Forecast

The plant based food market India 2026 or vegan diet trend isn't just growing. It’s essentially witnessing a significant momentum. We’re talking about a massive transition in how people eat, driven by health scares and a sudden, sharp realization that the planet is struggling. If we go by the numbers of Grand View Research, the India vegan food market generated a revenue of USD 1,124.5 million in 2026 and is expected to reach USD 2,826.5 million by 2033.. That seems like a structural shift.

What is Plant-Based Food?

So the term is pretty literal. It means food made from plants like grains, legumes, nuts, and seeds. But it’s more than just a pile of vegetables on a plate. The modern version of this is about technology. It has quite largely evolved into using things like peas or soy to recreate the taste and texture of meat and dairy or using their extracts to make supplements.

Why Plant-Based Food Market in India is Growing

1. Protein Shift

People are shifting from animal protein and are preferring alternate sources of plant based protein in India. There’s a massive move toward pea, soy, and rice protein India options right now. It’s not just for athletes anymore. It’s about feeling less bloated and actually knowing what’s on the ingredient label. Clean is the new standard.

2. Rising Vegan Awareness

Veganism isn't some niche liking for the elite anymore. In urban India, it’s gone completely mainstream. Social media started it, but now vegan FMCG India brands are finishing it by putting plant-based meat and dairy on every shelf. It’s accessible. It’s trendy. And it’s working.

3. High Lactose Intolerance in India

This is the "silent" driver. The data from SGPGI and the NIH is pretty staggering—about 60–74% of Indians can’t actually process dairy properly. Most people just lived with the discomfort before. Now? They’re just buying oats and almond milk. It’s a massive, built-in market that’s finally found a solution.

4. Climate & Sustainability Push

Let’s be real: the old way of eating is high-carbon. Consumers are waking up to that. But it’s the businesses, too. They’re pivoting to low-carbon food choices to hit those ESG goals before they get called out. It’s about survival—for the planet and the brand. In short, the market isn't a fluke. It’s a collision. Nutrition, necessity, and a ticking clock on the environment.

India Vegan / Plant-Based Food Market Segmentation

| Category | Leading Segment | Market Share |

|---|---|---|

| By Product | Dairy Alternatives | 46% |

| By Source / Ingredient | Soy | 34% |

| By Distribution Channel | Supermarkets & Hypermarkets | 41% |

Source: IMARC Group – India Vegan Food Market Report

Key Segments Driving the Vegan Food Market India

The market isn't just one big block. It’s fragmented into specific categories that are all moving at different speeds. Some are driven by necessity, others by pure lifestyle changes.

Plant-Based Protein India

It is worth acknowledging that demand for soy, pea, and rice protein is constantly surging. Indeed, it is no longer just a niche product that is confined to professional athletes. We’re seeing a massive shift where regular people are incorporating these into their daily nutrition to fill the protein gap. The gym culture in India is not major, but definitely among the factors here. People want high-quality protein. But they also want it to be easily digestible and, most importantly, easy to consume.

Plant Meat Market India

This is where the innovation is most visible. "Mock meat" and alternative chicken products are becoming standard. It isn't just about retail, though. Startups are driving the tech, but the real momentum is coming from the QSR (Quick Service Restaurant) sector when it comes to plant meat market India. Fast food chains are adding plant-based patties to their menus because the demand is there. It’s becoming a mainstream convenience.

Dairy Alternatives

This segment is probably the most established. Almond and oat milk are leading the charge. It’s a mix of people dealing with lactose intolerance and those who simply prefer the taste or the lower calorie count. What’s interesting is how quickly these have moved from specialty health stores to local supermarkets. They’ve become a staple. It’s a functional choice that has completely changed the dairy aisle.

Top Plant-Based Brands in India 2026

The market is crowded now, but a few names are doing the heavy lifting in plant based brands India 2026. These aren't just companies; they’re the ones actually putting products on the shelves that people want to buy. Here’s who you need to know.

- GoodDot: They’re essentially the pioneers here. Based out of Udaipur, they’ve managed to make plant-based meat affordable, which is a huge hurdle in India. Their "UnMutton" range is everywhere. It’s shelf-stable too, so you don't even need a freezer for half their stuff.

- Imagine Meats: This is the Bollywood entry. Founded by Riteish and Genelia Deshmukh, they’ve focused heavily on the "craveable" side of Indian cuisine—kebabs, biryanis, and curries. It’s smart. They’re targeting the flavor profile people actually miss when they go meatless.

- Blue Tribe: If you’re looking for that "bleeding" meat texture or high-end nuggets, this is it. They’ve gone big on the tech side to get the mouthfeel right. They’re very active in the urban D2C space and are pushing the sustainability angle hard.

- Urban Platter: Not just a "meat" brand. They’re more like the ultimate pantry for anyone living a plant-based life in India. From vegan cheeses to rare grains and oils, they’ve become the go-to for the "ingredients" side of the market.

- Epigamia: Known for yogurt, but their plant-based range—specifically the coconut and almond milks—is a structural part of the dairy-free movement. They’ve made it accessible. It’s in almost every major grocery store now.

Brand Comparison at a Glance

| Brand | Primary Category | USP | Price Range |

|---|---|---|---|

| GoodDot | Meat Alternatives | Shelf-stable & Affordable | ₹150 – ₹350 |

| Imagine Meats | Ready-to-Eat Meals | Authentic Indian Flavors | ₹300 – ₹600 |

| Blue Tribe | Alt-Meat (Frozen) | Realistic Texture & B12 enriched | ₹250 – ₹500 |

| Urban Platter | Gourmet Ingredients | Massive Variety (1000+ SKUs) | ₹200 – ₹1500+ |

| Epigamia | Dairy Alternatives | Creamy Texture & Availability | ₹100 – ₹300 |

Future Outlook & Challenges (2026–2033)

The road to that 2033 projection we looked at earlier isn't just a straight line up. It can’t be. We’re moving past the "novelty" phase where people buy a plant-based burger just to see what the fuss is about. Now, it has to become a habit. To actually hit those multi-billion dollar targets, the industry has to solve some very specific, grounded problems. It’s about moving from the early-adopter stage into the actual mass market.

Key Challenges to Overcome

It isn't all smooth sailing. There are real friction points that could slow things down if brands aren't careful.

- Price Parity: This is the big one. Right now, plant-based meat and dairy are often 2x to 4x the price of the real thing. It’s a luxury. For a middle-class Indian household to make the switch permanently, that price gap has to vanish.

- Taste & Texture: Humans are wired for familiarity. If a plant-based kebab doesn't "hit" the same way a traditional one does, people won't buy it twice. The tech is getting better, but perfecting the mouthfeel is still a work in progress.

- Cold Chain Logistics: Most of these products need to stay frozen or chilled. India's cold storage infrastructure is still catching up, especially once you move away from Tier 1 cities. If you can't keep it fresh, you can't scale. Simple.

Opportunities and Trends

Despite the roadblocks, the momentum is basically witnessing a significant shift due to some new players and actual institutional support.

- Govt & Biotech Push: We’re seeing more than just talk. The government is starting to invest in "BioFoundries" specifically to scale alternative protein. It’s about national protein security now.

- The Gen Z Factor: Roughly 35% of consumption spending in India is now coming from Gen Z. They care about transparency. They’re the ones actually reading the back of the package before they buy.

- Quick Commerce: Platforms like Blinkit and Zepto have changed the game. You can get oat milk delivered in 10 minutes now. This convenience is doing more for the market than any billboard ever could.

Import Trends in Plant-Based Protein India

India has a bit of a "protein paradox" going on. We are global leaders in producing raw pulses, yet when it comes to the high-value stuff—the actual protein isolates used in food tech—we are almost entirely reliant on other countries. The data from MOFPI is pretty blunt about it: India currently imports nearly 90% of its plant protein isolates.

It’s a massive gap. We have the raw materials, but we lack the domestic extraction and processing power to turn them into the powders and concentrates that brands need. This makes the entire sector heavily import-dependent. If you’re a startup in India making vegan meat, you’re likely sourcing your "magic ingredients" from abroad.

Key Imports and Global Sources (2024 Data)

The supply chain is surprisingly spread out if we look at the specific HS-code data for 2024. We aren't just buying from one place. In fact, we’re sourcing specific proteins from very different corners of the globe.

| Protein Category (HS Code) | Top 3 Exporting Countries to India | India's Share in Global Imports (%) |

|---|---|---|

| Soya beans (120190) | Niger, Togo, Benin | 0.29% (combined top 3) |

| Shelled Almonds (080212) | USA, Iran, Australia | 2.16% (combined top 3) |

| Wheat Gluten (1109) | China, France, Latvia | ~0.017% (combined top 3) |

| Dried Shelled Peas (071310) | Canada, Russia, Turkey | 1.22% (combined top 3) |

Source: MOFPI

Consumer Trends in Vegan Food Market India

Plant-based food in trend? It’s not just for the vegan followers anymore. That’s a myth. The reality is a lot more layered in the vegan food market India. We’re seeing the middle class move in now. Why? Because it’s practical. Many people are not able to handle the bloating that comes with dairy based protein. They want cleaner labels. They want to drink their tea without the lactose issues, but they aren't ready to give up the taste. It isn't a "lifestyle" statement for most of these people. It’s functional. Better digestion. Better health. Simple as that. It’s moving fast because it actually solves a problem.

Growth Drivers and Impact

The market is being pulled forward by a few specific levers. Some of these are hitting right now, while others are slow-burn structural changes.

| Driver | Impact on CAGR | Geographic Focus | Timeline |

|---|---|---|---|

| Government Initiatives | +1.5% | MP, Maharashtra, Rajasthan, UP | Long term (4+ years) |

| Processed Food/Retail | +1.3% | National (Organized retail & e-com) | Medium term (2–4 years) |

| Flexitarian Diets | +1.2% | Metros with spillover to Tier-2 | Medium term (2–4 years) |

| Lactose-Free Demand | +0.9% | Urban & Semi-urban | Short term (≤ 2 years) |

| Clean-Label Preference | +0.8% | Urban & Affluent segments | Short term (≤ 2 years) |

| Tech/R&D Innovation | +0.6% | Bengaluru, Pune, Hyderabad hubs | Long term (4+ years) |

Source: Mordor Intelligence

Tier 1 vs Tier 2 Demand

The geography of demand is changing. It’s not just a Mumbai or Delhi story anymore.

- Tier 1 Metros: This is where the "heavy" demand lives. Cities like Bengaluru, Mumbai, and Delhi are the primary engines, especially for flexitarians who are swapping out meat a few times a week. The infrastructure—quick commerce and specialty cafes—makes it effortless here.

- The Tier 2 Spillover: We’re starting to see significant traction in Tier 2 cities. It’s a different vibe, though. In these areas, the growth is often driven more by health necessity—like rising awareness of dairy intolerance—rather than just "lifestyle" choices. E-commerce is the bridge here. If a local store doesn't stock oat milk, people are just ordering it online.

The gender split in the Indian plant-based market is actually quite lopsided, but for reasons you might not expect. It isn't just about who is "healthier." It’s about how men and women perceive food differently in a culture where meat has some heavy baggage.

Gender Trends in Plant-Based Food (India 2026)

Men and women in India are buying into the plant-based movement for completely different reasons. If you look at the checkout counter, the intent behind the purchase tells two different stories.

Female Consumers: The Early Adopters

In India, women are currently the primary drivers of the "lifestyle" side of this market. Data from PBFIA and Ipsos suggests that women—especially in Gen Z and millennial cohorts—have a much more favorable outlook on going fully plant-based.

- The "Health-First" Mindset: For many Indian women, the shift is about preventive health and managing weight or digestion. They are more likely to spend extra on a "clean-label" almond milk or a vegan protein bar.

- Sustainability & Ethics: There’s a stronger emotional connection to the "climate" narrative. Women are leading the charge on ethical consumption, often being the ones who introduce these brands into the household pantry first.

Male Consumers: The Performance & Curiosity Gap

For men, the transition is a bit more complicated. There’s a long-standing cultural association between meat and "masculinity" that brands are still trying to break.

- The Protein Currency: When men buy plant-based, it’s almost always about performance. Think pea-protein shakes or high-protein mock meats after a workout. They aren't looking for a "salad"; they’re looking for a direct 1:1 replacement for chicken or mutton that doesn't mess with their fitness goals.

- The Novelty Factor: Men are actually more likely to try "meat mimics" like plant-based burgers or nuggets out of sheer curiosity or "tech-appeal" in a restaurant setting. It’s less about a moral shift and more about trying the latest food innovation.

Challenges in Plant-Based Food Industry India

The road for plant-based brands in India is far from smooth. It isn’t just about putting a product on a shelf. You’re fighting decades of eating habits and some very real economic walls. If this market is going to scale, these three hurdles have to be cleared. No two ways about it.

High Pricing

This is the elephant in the room. Right now, plant-based meat and dairy are basically luxury items. When a liter of oat milk costs three times more than regular buffalo milk, the average Indian household isn't making the switch. It’s a math problem. Until these brands hit economies of scale and bring prices down to parity, they’ll stay stuck in the "premium" urban bubble. It has to become affordable for the common man, not just the South Delhi or South Bombay crowd.

Taste Barrier

Indians are obsessed with flavor. We have a massive culinary heritage built on very specific textures—the "snap" of a kebab or the richness of dairy cream. Most plant-based products still struggle with what we usually would call "mouthfeel."

If it tastes like cardboard or has a weird aftertaste, people won't buy it a second time. Curiosity gets them the first time. Quality brings them back. Right now, the literal gap between "mimic" and "the real thing" is just kind of still a bit too wide and perhaps for immediate reach to the mass market.

Awareness Gap

There is a massive amount of confusion out there. A lot of people still think "plant-based" is just a fancy word for a salad. Others are suspicious of the "processed" nature of these mock meats—they see a long list of ingredients and get intimidated. Brands aren't just selling a product; they are having to educate an entire population on what this stuff actually is. It’s a slow burn. Without a massive push in consumer education, the "why" behind the shift remains a mystery to most.

Future of Plant-Based Food Market India

The next phase of this market isn't about being an "alternative" anymore. That’s the old way of thinking. Now? It's about being everywhere. We’re moving into a period where these options aren't just for the early adopters or the health-obsessed. They’re becoming a standard part of the Indian diet. No fanfare. Just a regular choice on the menu.

Mainstream Adoption

Expect to see "plant-forward" meals move way beyond the big metros. We’re already seeing Tier 2 and Tier 3 cities getting curious. It’s not about the vegan label anymore—it’s about the flexitarian lifestyle. People are realizing they don't have to be 100% vegan to make a difference. They’re just swapping out a meal here and there. This "normalizing" of the diet is what drives the real volume. By 2030, finding a plant-based kebab at a local wedding won't be a surprise. It’ll be expected. Simple as that.

FMCG Integration

This is where the real scale happens. Big players like ITC, Nestle India, and Tata Consumer Products are watching from the sidelines. They are actively pushing plant-based lines into their massive distribution networks. The game changes the second you can find a plant-based snack at your local kirana store. We’re moving from niche D2C brands to heavy-hitter FMCG presence. That means better prices. It means consistent quality. Most importantly, it means trust.

Export Potential

India has a massive, untapped advantage here. We are already an agricultural powerhouse, but the shift now is to stop just exporting raw pulses. We need to export high-value, processed plant proteins. Think about it. With our spice heritage and lower production costs, Indian "mock meat" with flavor profiles like tikka or cafreal has a massive market in the Middle East and Southeast Asia. We aren't just consuming this stuff. We’re going to be the ones supplying it to the world.

In today’s global trade environment, exporters increasingly rely on structured platforms that enable direct interaction with verified buyers across multiple countries. These systems streamline bulk trade by ensuring transparency in pricing, quantity, and payment processes, making it easier for suppliers to scale internationally. Register as exporter

Disclaimer

This article is for informational purposes only. Market size, growth projections, segmentation data, and industry insights are based on publicly available reports and estimates. Actual market conditions, pricing, and business opportunities may vary depending on economic factors, consumer trends, and regulatory changes. Readers are advised to verify details from official sources before making business or investment decisions.

Author

Pravarsh Sharma

Trade Expert, Tradologie.com

Pravarsh Sharma is directly involved in international trade facilitation and B2B commodity sourcing, helping global buyers and suppliers connect through structured trade ecosystems. His expertise lies in agro-commodities, FMCG trade, and cross-border business operations, making him actively engaged in real-world export-import dynamics.

-(1)converted.webp "Tradologie Reviews: Bridging Global Trade Gaps Through Technology")