Global bulk trade operates within an intensely competitive landscape. Profit margins are therefore often extremely narrow. Optimizing export pricing is therefore essential. Doing so requires a profound grasp of both domestic tax structures and government-provided incentives. The Remission of Duties and Taxes on Exported Products (RoDTEP) scheme stands out as one such critical mechanism. Its primary purpose is to protect Indian exporters from the disadvantage of unrefunded local taxes. Ultimately, the scheme functions as a pivotal tool for large-scale import-export operations. It proves particularly vital for businesses managing high-volume commodities

This is a comprehensive guide that will help you understand the RoDTEP scheme, make the most of its advantages, and incorporate it into your bulk trade plan.

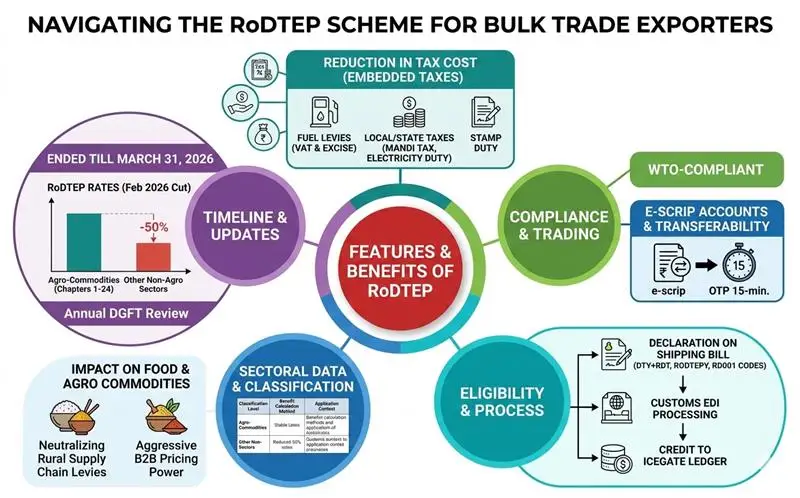

The RoDTEP scheme was introduced as a direct replacement for the Merchandise Exports from India Scheme (MEIS). This strategic shift was essential to ensure that India’s export policies stayed fully compliant with global trade norms. The initiative officially went into effect on January 1, 2021. It operates under a highly specific and clear mandate. Its core objective is to neutralize the embedded taxes and duties borne by exported goods. Specifically, it targets those levies that are not credited, remitted, or refunded through any other channels. The Indian Trade Portal provides clear guidelines on how the scheme is governed. It notes that while the Department of Commerce is responsible for notifying the scheme, the Department of Revenue actually handles its full administration.

For bulk exporters, this development marks a profound structural change. It shifts the industry away from arbitrary financial incentives and toward a much more precise, tax-neutralizing refund system.

In large-scale B2B exports, embedded taxes can significantly inflate the Free On Board (FOB) price of goods. The RoDTEP scheme addresses this by compensating exporters for hidden duties and levies at the Central, State, and Local levels.

As cited by official Department of Commerce guidelines, the scheme targets several specific un-refunded costs:

By reclaiming these hidden costs, bulk traders can offer far more competitive pricing in international markets.

A major advantage of the RoDTEP scheme is its inclusivity. The benefit is available to all exporters, regardless of their operational status, provided the goods are manufactured in India.

However, the Indian Trade Portal explicitly outlines several ineligible categories that traders must avoid to prevent compliance issues:

Understanding these exclusions is critical for bulk exporters who often manage complex, multi-origin supply chains.

Precision in product classification is the cornerstone of claiming RoDTEP benefits. The scheme categorizes products based on their tariff heading at an 8-digit level. Currently, the government has extended these benefits to an impressive 8,555 tariff items. To determine the exact rebate, exporters must consult Appendix 4R of the Handbook of Procedures.

The compensation structure varies depending on the product category, which is crucial for forecasting margins in bulk agro-commodities or raw materials.

| Classification Level | Benefit Calculation Method | Application Context in Bulk Trade |

|---|---|---|

| 8-Digit HS Code | Percentage of FOB Value | Standard for most bulk-manufactured goods and commodities. |

| Specific Tariff Items | Fixed Amount per Unit of Measurement (UQC) | Applied to certain standardized bulk volumes to prevent over-compensation. |

| Value Cap | Capped Rebate Amount | Limits maximum rebate per unit, regardless of total FOB value fluctuations. |

For high-volume bulk commodities, even a fractional percentage point in these rate structures can translate to millions of rupees in recovered margins.

Claiming these benefits requires meticulous documentation at the port of origin. The process is entirely digitized through the Customs Electronic Data Interchange (EDI) system. The lack of proper electronic documentation will render an export shipment ineligible, emphasizing the need for rigorous back-office compliance.

To avail of the scheme, an exporter must execute the following steps on the Shipping Bill:

Once Customs processes the eligible Shipping Bills and the Export General Manifest (EGM) is filed, a scroll is generated. The refund amount is then credited to the exporter’s ICEGATE portal account. Exporters must create a specific RoDTEP credit ledger account using their Importer-Exporter Code (IEC) and a Digital Signature Certificate (DSC).

These credits are issued as e-scrips. What makes these e-scrips highly valuable for the import-export ecosystem is their transferability. An exporter can easily transfer the e-scrip to another organisation with a valid IEC if they do not want to use it to pay Basic Customs Duty (BCD) on their own imports. This transfer process is protected by an OTP that is valid for precisely 15 minutes, according to ICEGATE security protocols, guaranteeing safe B2B digital transactions.

In order to optimise cash flow, platforms and businesses that facilitate large amounts of cross-border trade must use the RoDTEP scheme. The Foreign Exchange Management Act (FEMA) of 1999 stipulates that the sale proceeds must be received within a specific timeframe; if they are not, the rebate will be considered invalid. This is true even though the initial issuance of the rebate is not strictly dependent on the immediate realisation of export proceeds.

Furthermore, the Directorate General of Foreign Trade (DGFT) conducts annual reviews of the scheme. Industries that feel their specific bulk products are under-compensated can file formal representations before the Ministry for the next financial year. By integrating RoDTEP utilization into their core financial strategy, bulk exporters can effectively lower their cost basis, drive higher volumes, and maintain a formidable edge in global procurement markets.

Impact on Food & Agro Commodities

RoDTEP is a vital lifeline for the agricultural sector, especially for high-volume staples like rice, pulses (like lentils and pigeon peas), and specialty spices, in order to maintain global competitiveness. The strategic impact includes: