Key Highlights

The international grain trade has spent the last few seasons on edge, nervously watching weather maps and tracking policy shifts from major producing capitals. With El Niño weather patterns threatening to squeeze crop yields across several key agricultural regions, supply security has become a primary focus for procurement teams globally. Yet, while a significant portion of the global market prepares for a tight supply environment, the narrative unfolding across India's grain bins is shifting in a completely different direction.

Driven by exceptional domestic production and an intense state-backed buying cycle, India is currently sitting on an unprecedented mountain of rice. For global rice buyers, this massive inventory build-up represents a crucial supply anchor at a time when alternative origins are facing climate bottlenecks. This structural surplus doesn't just guarantee domestic food security; it sets the stage for a massive export cycle that could fundamentally steady global grain prices.

The Reality of an Overflowing State Reserve

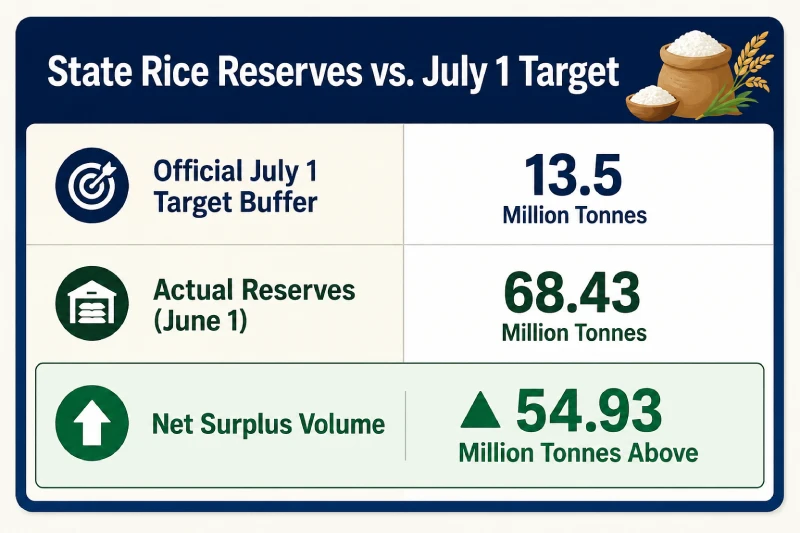

This supply security is anchored by an exceptionally heavy government procurement cycle. By early June 2026, state reserves—including unmilled paddy—hit a record 68.43 million tonnes. To place that in context, the government’s formal buffer target for July 1 sits at just 13.5 million tonnes. Warehouses are essentially holding more than five times the minimum required baseline, creating an unprecedented supply cushion.

This inventory growth stems from a highly efficient execution of the government's minimum support price (MSP) program. In the current 2025-26 marketing year, state agencies have already locked in 54.15 million tonnes of rice by early June, running comfortably ahead of the 51.16 million tonnes logged over the same timeframe last year.

With strong rabi and summer yields expected to extend the buying cycle straight through September, total state procurement is projected to top out at 58 million tonnes. Given that India’s baseline public welfare distribution requires roughly 40 to 42 million tonnes annually, the government is insulated against supply shortfalls. This safety net allows the state to support the open market and continue providing subsidized feedstocks to domestic ethanol distillers without risking its core food security buffer.

Why Global Rice Buyers Are Looking South

For global rice importers, the sheer volume of India's current stock reshape the procurement equation. In 2023, sudden rice export restrictions out of New Delhi sent shockwaves through international markets, squeezing supplies for dozens of dependent nations. But the current inventory landscape makes a repeat of those restrictions highly unlikely. The government has clear visibility on its domestic surplus, meaning trade routes are expected to remain open and predictable.

Furthermore, commercial economics heavily favours Indian origins. Relatively soft local wholesale rates, combined with a recent softening of the Indian rupee against the US dollar, have left Indian grain highly competitive against competing supplies from Thailand, Vietnam, and Pakistan.

While actual shipments through April 2026 started the marketing year systematically slower at 13.4 million tonnes, export velocity has picked up significantly since February. If trading houses maintain their current run rate of moving roughly 2 million tonnes per month, total shipments for the current cycle will easily reach a record-breaking 23 million tonnes. Looking further out into the 2026-27 marketing window, the USDA projects that this competitive pricing model will push India's total volume to an all-time high of 25 million tonnes.

Commercial Repercussions for Trading Houses

For trading enterprises built around the ability to export rice in bulk, this supply cycle represents a highly favorable trading window. The baseline risk of sudden policy interventions or export freezes has dropped significantly because domestic state reserves are so secure. This regulatory stability gives exporters the confidence required to negotiate larger, long-term supply contracts with international buying desks rather than just operating in volatile spot markets.

The market is also seeing a healthy expansion in private stocks. Inventories held by private trade entities and exporters are projected to climb to 4 million tonnes, up from 3.1 million tonnes last season. When combined with state reserves, India’s total year-end closing stocks for the 2025-26 cycle are on track to touch an unprecedented 54 million tonnes.

This means that whether a trading desk is looking to move standard non-Basmati white rice or specialize in premium parboiled volumes, the physical grain is readily available at highly predictable price points.

Reshaping Global Price Movements

Ultimately, India’s return to a high-volume rice export footprint serves as a critical stabilization tool for the wider agricultural economy. Because India commands an absolute 40% share of the international rice market, any major shift in its domestic volume immediately dictates terms to the rest of the world.

The massive wave of Indian grain moving into global channels will act as an effective price ceiling, helping cool off global food inflation and calming supply anxieties across import-dependent nations. For businesses looking to sell rice globally, the message is clear: India is entering one of its most dominant supply cycles in recent history, merging unmatched production scales with an aggressive logistical edge to solidify its position as the ultimate anchor of the global grain trade.