Key Highlights

- Most wheat in global trade moves under HS Code 1001. Sounds technical, but in real deals this decides duties, documentation, and how fast your cargo actually clears. Small mistake, big headache.

- The market is already around USD 196 billion and heading toward USD 270 billion. No hype. Just steady demand because wheat is basic. People don’t stop eating bread, noodles, or biscuits.

- Export control today sits with a few countries, while big producers like China, India, Russia keep most wheat at home. That’s why supply suddenly tightens in the global market even when production looks strong on paper.

- Smart buyers now spread risk. One origin is never enough. Backup suppliers, multiple regions, and consistency matter more than saving a few dollars per ton.

Introduction:

Let’s be honest. Wheat is not exciting as ready to eat packed food products. Nobody wakes up thinking about wheat. It doesn’t trend. It doesn’t dominate headlines. But remove it for a few weeks and the entire food system starts shaking. That’s the reality.

This has been true for thousands of years. The first big civilisations didn’t rise because of technology or capital. They rose because they figured out how to grow and store grain. Wheat meant stability. Stability meant power. Whoever controlled grain controlled society. That logic still works today. Just the scale has changed.

Today, the global wheat market is worth close to USD 196 billion. It is expected to cross USD 270 billion by the end of the decade. No sudden spikes. No dramatic crashes. Just slow, steady growth. And that is exactly why wheat is dangerous to ignore. It moves quietly. But it moves everything.

👉 See complete HSN Code List for global commodity trade.

So who is actually producing all this? Keep reading this informative piece of blog as it will tell you in detail about the top 10 wheat producing countries globally.

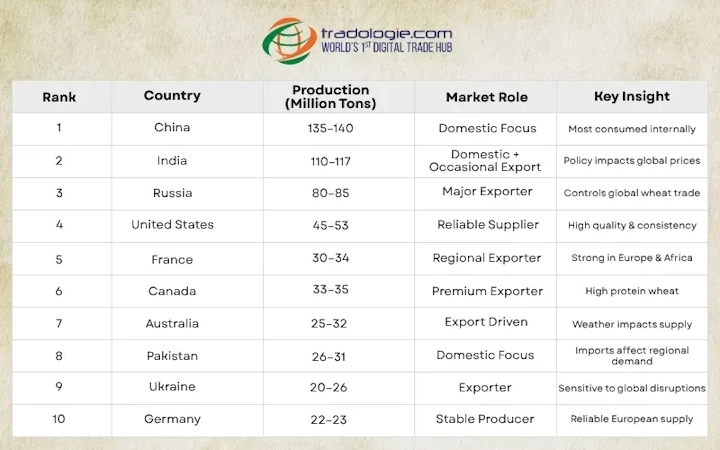

1. China (around 135–140 million tons)

China sits at the top when it is about the top 10 wheat producing countries. Not even a competition. Around 135 to 140 million tons every year.

But here is the thing. China is not playing the export game. Most of this wheat never leaves the country. It goes straight into domestic consumption. The goal is simple. Feed the population. Control inflation. Avoid social instability.

It’s not glamorous. But it works. When your domestic system is strong, global volatility matters less.

2. India (around 110–117 million tons)

India is next. Somewhere between 110 and 117 million tons.

Again, domestic consumption dominates. Public distribution systems, government procurement, food security. This keeps the system stable.

But India behaves differently in global trade. It enters when there is surplus. Then suddenly disappears. Markets don’t like uncertainty. That’s why wheat traders track India closely. A policy change here can move prices overnight.

3. Russia (around 80–85 million tons)

Now we come to the real disruptor. Russia.

Around 80 to 85 million tons. But more importantly, aggressive exports. Africa, the Middle East, Asia. Russia is everywhere.

Low cost. Large volumes. Strategic positioning. Over the last decade, Russia has quietly taken control of the export narrative. These days, if you want to understand price direction, you watch Russia first.

Everything else comes later.

4. United States (around 45–53 million tons)

The US is playing a different game.

Production sits around 45 to 53 million tons. But the focus is not volume. It is consistent. Food companies want predictable flour. Bakers want stable gluten. Industrial buyers want fewer surprises.

So the US positions itself as a reliability supplier. Not the cheapest. But dependable.

And in food, dependability often wins.

5. France (around 30–34 million tons)

France is Europe’s backbone and is on the fifth number in top 10 wheat producing countries.

Production stays between 30 and 34 million tons. Strong infrastructure. Efficient logistics. And most importantly, geography. North Africa depends heavily on French wheat.

Sometimes distance matters more than price. Freight decides competitiveness.

6. Canada (around 33–35 million tons)

Canada is not chasing mass markets.

Around 33 to 35 million tons. But premium quality. High protein. Strong milling characteristics. Pasta and bakery industries prefer Canadian wheat.

It sells less volume than some others. But often at better margins.

7. Australia (around 25–32 million tons)

Australia is export-focused. Production fluctuates between 25 and 32 million tons.

But the real driver is weather. One good season, supply floods global markets. One bad year, prices shoot up.

This unpredictability makes Australia important. Wheat traders build strategies around it.

8. Pakistan (around 26–31 million tons)

Pakistan produces roughly 26 to 31 million tons.

Mostly consumed domestically. But whenever output drops, imports rise. That changes regional demand. South Asian markets feel the impact.

Sometimes importers shape the market as much as exporters.

9. Ukraine (around 20–26 million tons)

Ukraine has long been called the breadbasket.

Production usually sits between 20 and 26 million tons. But recent disruptions have shown something important. Global supply chains are fragile. Even small shocks from Ukraine move prices.

The world is interconnected. Whether it likes it or not.

10. Germany (around 22–23 million tons)

Germany is steady. Efficient. Predictable.

Around 22 to 23 million tons. Not aggressive in exports. But reliable inside Europe.

And in commodities, reliability is currency.

So What Does This Actually Mean?

This is not just a ranking. It is a strategy map.

- Some countries focus on feeding their population.

- Some dominate exports.

- Some build premium positioning.

- Some strengthen regional influence.

At the same time, buyers are changing. Nobody wants dependence on one origin anymore. Climate shocks, geopolitics, logistics disruptions. All of this has forced diversification.

Multi-origin sourcing is becoming standard.

👉 See Complete IEC Code List for Indian Import Export Businesses.

The Road Ahead

Demand will rise. Population growth makes that inevitable. Processed food consumption will expand. Urban lifestyles will push wheat demand even further.

But supply will remain uncertain. Climate volatility, policy risks, and geopolitical tension will shape the future.

The winners will not just produce more. They will build systems. Storage. Logistics. Compliance. Partnerships.

Because in global wheat trade, scale gets attention.

Consistency gets contracts.

And contracts build long-term power.