Why Africa Is Becoming a Strategic FMCG Market for Indian Exporters

Key Highlights

- Africa’s FMCG and foodservice market is projected to reach USD 79.81 billion in 2026.

- The market is expected to grow to USD 102.43 billion by 2031.

- Africa’s FMCG sector is forecast to grow at a CAGR of 5.12%.

- Urbanization and retail modernization are accelerating demand for packaged products.

- Biscuits, snacks, instant foods, beverages, and personal care products offer strong export potential.

- South Africa, Kenya, Nigeria, Ghana, and Tanzania are key FMCG import markets.

- Private label manufacturing is creating new opportunities for Indian exporters.

- Organized retail expansion is increasing demand for branded and packaged FMCG products.

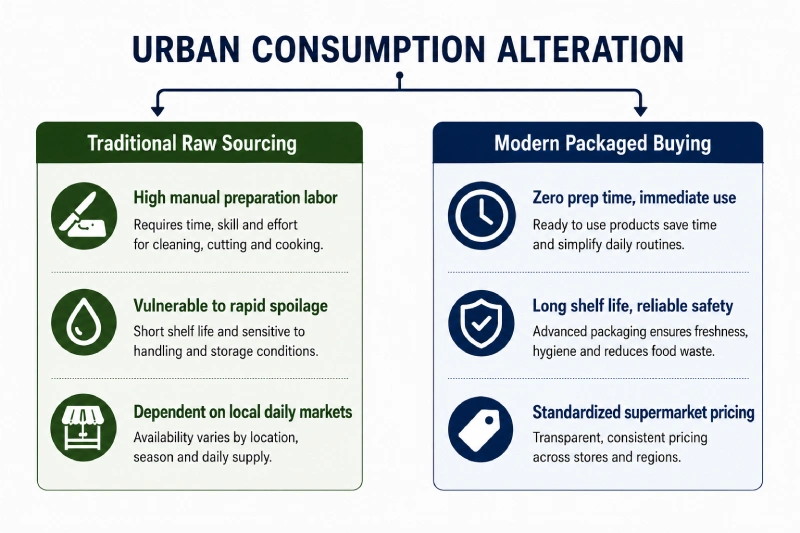

Organized retail channels are expanding across major regional hubs at an impressive rate, signaling that Africa's consumer landscape is entering a highly dynamic phase. Rapidly growing urban populations, paired with a general consumer migration toward premium, packaged alternatives, are altering traditional wholesale habits across sub-Saharan territories. For consumer goods manufacturing desks, these structural adjustments mean thinking beyond classic low-margin raw grain drops. The focus is shifting toward branded consumer product lines.

The value of unmanaged, loose wholesale networks will continue to decline as technology continues to bridge the connectivity gap between urban factories and village Kirana storefronts. True commercial longevity and sustainability belong to consumer brands whose distribution systems are backed by assets and monitored by technology and can regularly service the farthest corners of the country. FMCG enterprises can secure a premium, dominant position across the world's most active rural consumption frontier by deploying automated route systems, maintaining clear stock visibility, and designing pricing structures that match rural household budgets.

Capturing long-term volume loops in the FMCG export India to Africa pipeline requires a firm grasp on regional distribution routes and deep strategic insertion into the India Africa FMCG trade framework.

What's Changing in Africa's Consumer Goods Market?

Supermarkets, hypermarkets, and suburban convenience mini-marts are systematically reshaping how everyday households purchase grocery essentials. According to modern urbanization observations by the World Bank, the continuous movement of populations into capital cities is driving an immediate requirement for standardized, shelf-stable consumer items. This behavior changes everything for a traditional importer. When open-air wholesale yards yield space to formal corporate retail rows, unbranded bulk grains lose ground to trace-verified, packaged commodities.

Sourcing data shared by the African Development Bank points out that modern retail expansion is pulling formal distribution networks straight into secondary towns. For international suppliers, this infrastructural transformation is critical. Buying offices representing these new supermarket chains cannot buy unvetted open-market crops because their inventory tracking systems require barcodes, uniform pallet sizes, and predictable manufacturing dates. Exporters who pivot early to deliver shelf-ready, consumer-branded packages can secure predictable volume contracts with regional wholesale aggregators.

Market Size and Growth Outlook

Volume demand across this corridor is displaying a highly steady trajectory. Tracking the exact metric footprint of this territory highlights a reliable, long-term procurement environment for international manufacturers.

The broader baseline values of this consumer market can be broken down through recent industry indicators:

| Financial Metric | Absolute Value Layer | Sourcing Implication |

|---|---|---|

| Market Size Baseline (2025) | USD 75.92 Billion | Establishes a heavy consumption floor for entry brands |

| Market Size Baseline (2026) | USD 79.81 Billion | Current operational yardstick for tracking container flows |

| Projected Market Valuation (2031) | USD 102.43 Billion | Confirms multi-year institutional procurement expansion |

| Expected Compound Annual Growth (CAGR) | 5.12% | Sustained volume security for factory lines |

Source: Mordor Intelligence - Africa Foodservice Market Industry Report

What these figures suggest to a trade desk is a steady, predictable expansion of purchasing capacity rather than a sudden, volatile spike. Reaching a multi-billion-dollar valuation proves that urban consumption is pulling more product lines into formal retail every single year. FMCG suppliers can utilize these stable indicators to justify long-term investments in dedicated production runs, custom label printing, and specialized regional distribution setups.

Why India Is Emerging as a Preferred FMCG Sourcing Partner

Competitive manufacturing infrastructure gives Indian processing plants a significant operational edge when negotiating international supply deals. Value-tier formatting is a core strength of South Asian production lines, allowing mills to deliver highly reliable goods without pushing retail costs past regional income limits. For African buying groups, sourcing from this corridor ensures excellent scalability and long-term volume reliability.

Private label capabilities represent another major factor driving the growth of India food brands Africa lines. Large-scale retail chains in emerging economies want to scale up their in-house store brands to maximize gross margins. Indian factories can easily adapt their automated clean-room wrapping lines to print custom distributor labels, accelerating overall velocity across the India Africa FMCG trade lane. This production flexibility, paired with extensive deep-water shipping experience, positions Indian suppliers as highly competitive alternative partners to traditional, high-cost European exporters.

Which FMCG Products Have Strong Potential in African Markets?

Consumption patterns are zeroing in on product lines that combine high shelf stability with simple, rapid preparation. Bulk ingredients are seeing lower growth percentages, while value-added, processed categories command steady interest from corporate procurement managers.

Reviewing the baseline shipments moving through major deep-water ports reveals a highly diversified opportunity landscape:

High-Potential FMCG Categories

| Product Category | Opportunity Level | Core Distribution Target |

|---|---|---|

| Biscuits & Cookies | High | Urban retail shelves and modern convenience chains |

| Packaged Snacks | High | High-turnover impulse racks and school-lunch segments |

| Instant Foods | High | Ready-to-cook noodle runs for time-conscious buyers |

| Tea & Beverages | High | Premium breakfast blends and small sachet tea lots |

| Spices & Seasonings | High | Industrial processing facilities and household packs |

| Dairy Alternatives | High | Emerging plant-based retail segments in hub cities |

| Confectionery | Strong | Value-tier candy lines for high-volume trade routes |

| Personal Care Products | Strong | Mini-size hygiene lines, daily soaps, and shampoos |

| Household FMCG Products | Strong | Compact detergent bars and laundry powders |

Source: Trade Performance Analytics & Sourcing Blueprints 2026

Urban consumers are driving this selection shift. Time constraints increase the value of convenience-oriented buying patterns, when a family transitions to modern city employment. Products like instant noodles, biscuits that are portion-controlled, and small hygiene sachets fit seamlessly into these new urban routines.

How Sweet Biscuits Reflect India's FMCG Export Opportunity

Value-added food exports find an excellent operational example in the humble bakery segment. According to trade tracking details highlighted by the Department of Commerce, Indian sweet biscuits are steadily expanding their presence across global markets, including emerging regions. This specific segment is worth paying attention to because it bypasses the logistical vulnerabilities that usually hamper raw agro shipments.

Sweet biscuits are highly shelf-stable, meaning they handle long sea voyages and multi-tier regional warehousing loops without requiring expensive cold-chain infrastructure. This durability is exactly what makes them a perfect fit for the packaged food export Africa pipeline. By utilizing automated high-speed baking lines, Indian factories can continuously produce mass-market products that hit precise consumer price preferences across the branded food Africa market. This sector proves that converting simple wheat flour and sugar inputs into high-value, branded consumer packages delivers significantly more stable returns than bulk commodity trading.

Which African Countries Offer the Strongest FMCG Potential?

Distribution desks must analyze regional infrastructure variations before allocation planning, as import dependencies and port efficiencies differ wildly across geographic zones. Sourcing networks typically structure their regional hubs around clear corporate gateway countries.

The strategic drivers behind major regional import destinations can be mapped across several core territories:

Key African Markets for FMCG Exporters

| Country | Opportunity Driver | Strategic Commercial Role |

|---|---|---|

| South Africa | Organized Retail | Dominates high-end supermarket penetration across the continent |

| Kenya | Regional Hub | Functions as the single logistical gateway for the East Africa trade zone |

| Nigeria | Consumer Base | Represents immense volume scale due to a massive urban population |

| Ghana | Rising Middle Class | Offers highly predictable financial structures and steady retail demand |

| Tanzania | Urban Growth | Driving fast-paced retail modernization across coastal terminal lines |

| Ethiopia | Urban Population Growth | Massive domestic consumer pool transitioning into processed goods |

| Uganda | Regional Distribution | Key secondary inland distribution lane for landlocked trade spaces |

| Zambia | Increasing FMCG Imports | Growing reliance on value-tier branded personal care and food cargo |

Source: Regional Infrastructure Profiles & Procurement Logs 2026

Targeting these FMCG export Africa countries requires a tailored approach. South African buyers expect highly premium packaging aesthetics and strict microbiological assays. Conversely, entry into East or West African trade zones relies heavily on price access, clean clearing documents at port terminals, and reliable supply continuity.

How Retail Modernization Is Changing FMCG Demand

Regional distributors and large corporate wholesale chains are transforming how products pass from cargo holds to local shelves. Modern trade networks operate on a completely different set of procurement rules than traditional spot brokers. When a supermarket group builds out regional fulfillment centers, the buying office demands standardized products, uniform batch consistency, and damage-resistant packaging layouts.

This trend changes the game for international suppliers. Reliable tracking data shows that formal hypermarkets actively prioritize branded products because consumer recognition drives automated, high-velocity shelf turnover. Working with reliable suppliers who can guarantee uncompromised batch-to-batch quality ensures that these major chains avoid empty shelves, protecting their localized retail margins.

Packaged Food Export Africa: Why Demand Is Rising

Urban lifestyles are accelerating the shift toward preserved and easy-to-prepare meal formats. In major metropolitan centers, changing family structures mean that multiple household members are entering the workforce that leaves significantly less time for traditional scratch cooking. This domestic evolution is a core driver pushing the packaged food export Africa pipeline forward.

Shelf-stable foods, ready-to-eat noodles, and portioned snacks are no longer viewed as luxury additions. They have transformed into daily operational necessities for urban workers. For international suppliers, this structural trend provides a highly dependable volume lane, since consumer preference for clean, safely sealed nutrition lines remains insulated from temporary macroeconomic shifts.

What Exporters Should Consider Before Entering African Markets

Navigating this international trade route requires a practical, risk-managed approach to clear operational bottlenecks. Payment security stands out as a critical baseline factor, making the use of confirmed, irrevocable Letters of Credit (LC) standard practice for protecting corporate trade capital. Establishing close partnerships with verified regional distributors who understand local custom clearance channels is equally vital for preventing terminal delays.

Product adaptation represents another necessary operational hurdle. Label designs must comply with regional language laws, often requiring bilingual formatting or explicit nutritional adjustments to clear border safety gates. Packaging materials must be ruggedly engineered to handle high ambient heat and bumpy inland transport routes, ensuring that goods reach the final point-of-sale row in perfect condition.

Long-Term Opportunities for Indian FMCG Manufacturers

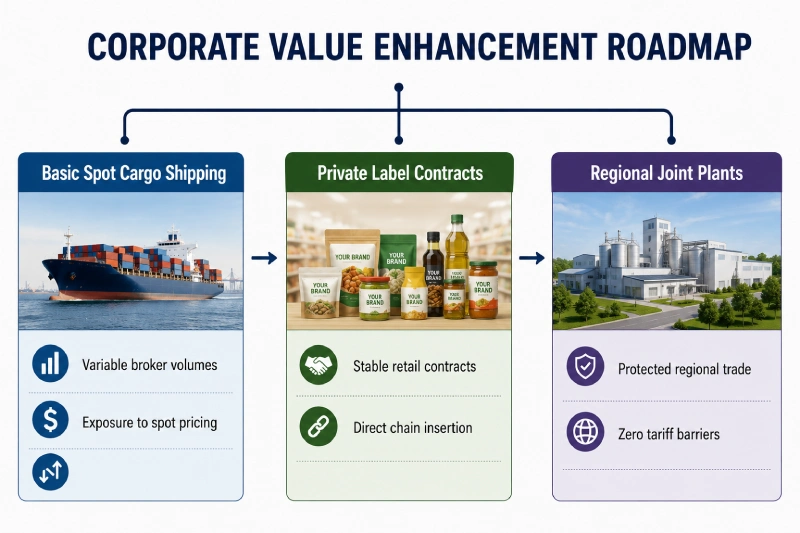

Agribusiness groups can discover excellent structural paths forward by moving past simple transaction-based container shipping. Building long-term market access relies heavily on entering into private label manufacturing agreements with dominant African supermarket networks. This strategy embeds your factory production directly into the daily supply loops of major corporate retailers.

Collaborating with localized food processing operations to establish joint packaging facilities within regional trade zones represents another high-return opportunity. By shipping raw bulk concentrates or semi-processed bases from India and handling final consumer packaging locally, firms can bypass import tariffs and benefit from regional trade agreements. These strategic moves help transition India food brands Africa lines into permanent fixtures within the evolving branded food Africa market.

What Africa's FMCG Growth Indicates for Exporters

The long-term consumption trends point to clear and sustainable market expansion. If one analyzes the broad revenue projection—where the market scales up from a USD 75.92 billion baseline to an estimated USD 102.43 billion by 2031—it proves that sub-Saharan purchasing power is transforming structurally. Tracking a steady 5.12% compound annual growth rate confirms that consumer demand is consistently outrunning local agricultural processing capacities.

For a trade desk, these numbers indicate a reliable, long-term requirement for diversified imports. This growth pattern isn't just about shifting higher volumes of basic goods; it shows an active consumer transition toward premium, value-added alternatives. AG-processing firms that invest in automated sorting machinery and high-barrier packaging arrays are backed by a multi-billion-dollar consumption wave that will continue to reshape North American and South Asian trading patterns for decades.

Conclusion

Succeeding in the modern FMCG export India to Africa corridor requires balancing commercial flexibility with complete regulatory discipline. The expanding African retail ecosystem offers exceptional long-term volume loops, but it remains accessible only to suppliers who prioritize consistent batch packaging and absolute supply continuity.

As formal retail formats continue to scale up across major gateway hubs, the commercial value of unverified, loose spot brokering will continue to decline. True corporate longevity belongs to asset-backed manufacturing firms that align their workflows with the exact inventory needs of regional supermarket groups. By optimizing logistics loops, locking down clear private label channels, and structuring pricing metrics around urban household budgets, Indian agricultural enterprises can secure a premium, dominant foothold across the India Africa FMCG trade landscape.